Hogan Steel Archive

Introduction

The “Hogan Steel Archive,” representing a three-year collaborative effort of the Walsh Library’s Department of Archives and Special Collections and Fordham’s Industrial Economics Research Institute, commemorates and preserves the remarkable steel legacy of the late Rev. William T. Hogan, S.J. (1919-2002), who came to be known the world over as the “Steel Priest.”

During a distinguished 52-year teaching career here at Fordham, Father Hogan earned well-deserved recognition as a true innovator in economic education and taught generations of students about industrial interdependence and the steel industry’s vital role in economic and industrial development. Created in Father’s honor, the Hogan Steel Archive transforms the invaluable steel information he assembled during his life’s work into a permanent educational resource for use by students, researchers, scholars, and all those seeking knowledge about the domestic and world steel industries.

Administered by Walsh Library and the Department of Economics, the Archive carries forward Fordham's longstanding tradition, established by Father Hogan, as a leading center for steel-industry information.

The Archive contains thousands of steel-document files, hundreds of books and photographs, and an extensive collection of international steel references and statistics, together comprising a uniquely comprehensive resource for learning about steel. The Archive’s content was categorized and annotated with respectful memory of Father Hogan by his longtime Fordham colleague, Frank T. Koelble, who also authored the content for this website. The Archive resides at the Walsh Library’s Department of Archives and Special Collections; was cataloged there by a dedicated team of student assistants, headed by Thomas Raj, Nancy Rinaldi, and Kerriann Barry; and benefited from the expertise of Fordham archivists Patrice Kane and Vivian Shen. The website was constructed by Michael Considine and Yuqing Zhang of Walsh Library's Electronic Information Center.

The success of this endeavor is testimony to the thoughtful generosity of Father Hogan’s family, friends, steel colleagues, and steel companies from around the world, whose participation in honoring Father is profoundly appreciated.

Biography

Born in the South Bronx on April 30, 1919 , William Thomas Hogan was a product of the Bronx public schools, P.S. 72 and James Monroe High. During the Depression, he delivered The Bronx Home News to help support his family and then pay his tuition at Fordham, where he would graduate college cum laude and eventually earn an M.A. in economics and, after becoming a member of the Society of Jesus, a Ph.D.

In the late 1940’s, his doctoral studies took him to Pittsburgh, then the nation’s and the world’s steel capital, where he lived at Duquesne University and worked at United States Steel Corporation in researching his dissertation on steel productivity. It was the first detailed study on the subject ever made, and his methods of productivity measurement were adopted by the U.S. Department of Labor and were detailed in his first book, Productivity in the Blast-Furnace and Open-Hearth Segments of the Steel Industry. Published in 1950, the book would forever identify Father Hogan with steel.

Also in 1950, Father founded Fordham’s Industrial Economics Research Institute (IERI) and initiated an interrelated research and teaching program in Industrial Economics. The innovative curriculum he developed served as a model that in time was integrated into the economics courses of 112 colleges and universities throughout 30 states and the District of Columbia. His curriculum also was adopted to educate the nation’s clergy about the history and workings of the U.S. economy’s industrial sector, and in 1954, his lectures were published in his second book, The Development of American Heavy Industry in the Twentieth Century, which became the text used by generations of students.

Father Hogan’s innovative teaching approach employed concrete examples drawn from everyday events in business and industry to not only demonstrate industrial interdependence, but also to give the student an appreciation of the size and complexity of basic heavy industry and of the labor and capital inputs needed to sustain its operation. The educational value of this approach was that in his words: “It provides a supplement to courses in economic theory, and thus gives students more opportunity to check theoretical principles against real-world business practices.”

Students first encountering Father Hogan in class were intrigued by the red-haired Jesuit’s well-tailored clerical garb, by his sharply creased trousers and well-shined shoes that were more akin to a corporate executive than a college professor. And then they watched in awe as he introduced his subject for the day while filling the blackboard with columns of statistics, all without ever consulting his notes. With commanding presence and in resonant tone, hinting of his talents as an Irish tenor, he would deliver an engaging and well-structured lecture, typically dealing with the economic basis for adopting some well-described steel or other technology, which he discussed both in historical context and by reporting his first-hand knowledge of the factors behind contemporary corporate decisions on the subject.

Over the years, both at Fordham and as a visiting professor at Penn State, Purdue, and Loyola, Father Hogan taught about the interdependence of the steel, automobile, railroad, petroleum, and utility industries and kept his course content current by means of research conducted by the Industrial Economics Research Institute, often with the participation of student interns, who were able to learn first hand just how basic heavy industry functions. Much of the Institute’s research demonstrated the pivotal role of the steel industry as a catalyst for economic development, and throughout his career, Father used his knowledge and worked tirelessly to foster international cooperation and understanding in the steel business, gaining his worldwide reputation as the “Steel Priest.”

From the late 1950’s through the early 1970’s, Father devoted considerable time and effort to studying the economic impact of the depreciation-tax laws on steel and other industries that rely on long-lived equipment, emphasizing the need for reforms to spur capital investment. He was instrumental in achieving passage of the investment-tax credit and other reforms proposed by President Kennedy, testifying on the subject on numerous occasions before legislative committees of the U.S. Senate and House of Representatives. In 1962 and 1967 he published his third and fourth books, Depreciation Reform and Capital Replacement and Depreciation Policies and Resultant Problems

In the late 1960’s, he served as a member of President Nixon’s Task Force on Business Taxation and was a consultant to the Council of Economic Advisors to the President. In all, he counseled five U.S. presidents on tax and steel matters and served as an advisor to many federal, state and local government agencies.

In 1971, Father Hogan’s landmark, five-volume work on the American steel industry was published. Having been in preparation for more than 15 years, his Economic History of the Iron and Steel Industry in the United States examines industry developments from 1860 to 1971. Father periodically updated his five volumes with a series of companion books: The 1970’s: Critical Years for Steel, 1972; World Steel in the 1980’s: A Case of Survival, 1982; Steel in the United States: Restructuring to Compete, 1984; Minimills and Integrated Mills: A Comparison of Steelmaking in the United States, 1987; Global Steel in the 1990’s: Growth or Decline, 1990; Capital Investment in Steel: A World Plan for the 1990’s, 1992; and Steel in the 21 st Century: Competition Forges a New World Order, 1994.

Father’s last two books were The Steel Industry of China: Its Present Status and Future Potential, published in 1999, and The POSCO Strategy: A Blueprint for World Steel’s Future, published in 2001 within months of his passing. His final book reflects how greatly he admired the success of the Korean people in starting from virtually nothing to build the world’s leading steel company. During the prior two decades, he had traveled to Korea every year to visit POSCO, to lecture on world steel, and to watch as his friend, Chairman Tae-joon Park and his successors so effectively put into practice his lifetime of teaching about steel’s key role in economic development, an experience that was among the most rewarding of his accomplished steel-industry career.

Undeterred by serious health concerns dating from the 1970’s, Father visited most of the world’s steel-producing facilities, delivered papers at conferences, and advised many steel managements. He had the distinction of having attended every annual meeting in what was then the 34-year history of the International Iron and Steel Institute, which named him one of only two honorary members.

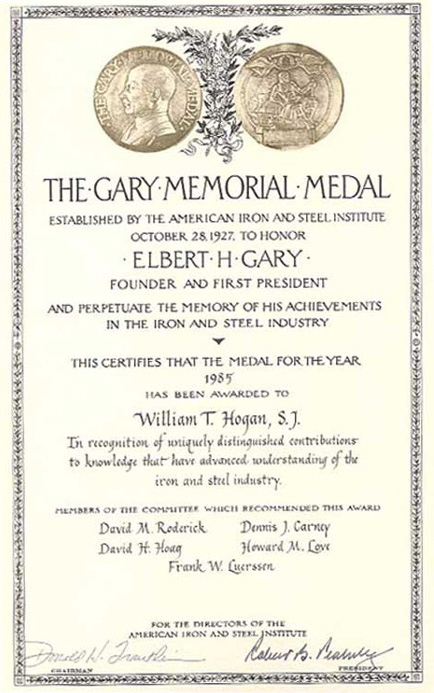

In 1985, the American Iron and Steel Institute awarded him the Gary Memorial Medal, the industry’s highest honor, otherwise given only to top steel executives. The medal was presented in recognition of “uniquely distinguished contributions to knowledge that have advanced understanding of the iron and steel industry.”

In 1987, Father was made a Distinguished Life Member of the American Society of Metals, and in 1990, the Association of Iron and Steel Engineers established the William T. Hogan Annual Lecture Series. In 1992, Korea ’s President Roh Tae-woo presented him with the prestigious Gold Tower of the Order of Industrial Merit, the highest business award the Korean government bestows. In 1995, he was awarded Honorary Membership in the Korea Iron and Steel Association. And finally, in 1996, he received his most recent degree, an honorary Doctor of Laws from his beloved alma mater, Fordham.

In profiling Father Hogan for Company magazine, Father George McCauley, one of his fellow Jesuits wrote as follows: “The New York Times got it wrong when it called him the ‘Boswell of the steel industry.’ He was its Johnson not its Boswell. He had a vast, direct knowledge of the industry’s intricate workings, from the smelter crews, ironmakers and sheet rollers he’d meet on the mill floor to executives who welcomed him into their lofty offices. He had shrewd insight into the directions available to the industry in the shifting circumstances of supply and demand and in times of fierce international competition. Miraculously, he had the trust of both steel producers and steel importers. Government officials, too, knew they were getting the real goods whenever Father Hogan came before them.

“For all that, the Steel Priest lived up to both sides of that facile sobriquet. His black suit and Roman collar seemed welded to his skin, probably turning a few heads in some circles he traveled.” But knowing the power of steel, he “ saw his work as a way of getting people out of their hopelessness – building lives, putting a little security and dignity within their reach.” At 82 years of age, having taught his final class and having celebrated his final book in December of 2001, Father Hogan passed away on January 12, 2002 , a teacher and steel man to the end.

The Hogan Steel Archive

The Hogan Steel Archive is comprised of the above five major sections, which provide structure and accessibility to its extensive and diverse content of steel documents, photographs, studies, personal papers, correspondence, books, references, and statistical information. This archival content was collected by Father Hogan starting in the late 1940’s, and by Father and his associates at the Industrial Economics Research Institute starting in 1950, and is the product of research performed in publishing more than 25 books, in preparing hundreds of articles and speeches, and in conducting more than 150 studies on various aspects of the steel industry and interrelated industries. The content includes 4,823 document files, 1,114 steel photos and slides, and 390 book and reference titles, most of which span the period 1850 to 2001 and encompass economic, technical, and historical information, much of which is not available anywhere else, making the Hogan Steel Archive a unique resource for steel education.

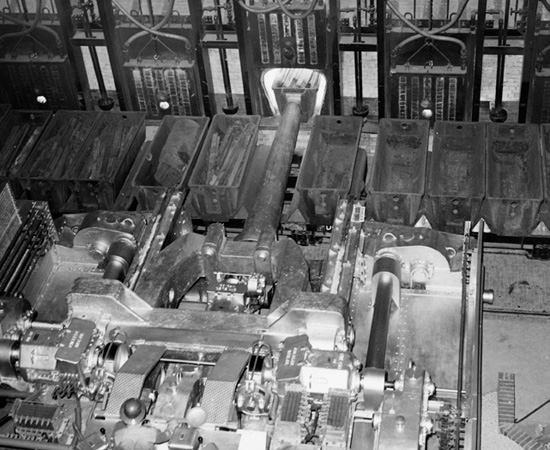

World Steel Files

The “World Steel Files” section of the Archive, representing its largest, consists of 55 archival boxes containing 3,917 document files on the following major steel and steel-related subjects: capacity and production, coking coal, companies in the U.S., countries producing steel, energy, environment, iron ore, labor, markets for steel, minimills, productivity, scrap, service centers, stainless steel, steel technology, taxes and depreciation, and trade. Descriptive summaries of the archived information for each subject category are provided below, in most cases accompanied by an instructive analysis and supportive photographs from the Archive’s photo collection.

Capacity and Production

The Archive contains 24 document files on steel capacity and production in the United States and on a world basis, as well as for selected countries, companies, plants, processes, and finished steel products. The steel industry’s long-term growth and development can be traced from data and information in these files, some dating from 1849, and from various statistical and other references elsewhere in the Archive, including the Annual Statistical Report and Iron and Steel Works Directory of the American Iron and Steel Institute (AISI); the Directory, Iron and Steel Plants of the Association of Iron and Steel Engineers (AISE); the Steel Statistical Yearbook of the International Iron and Steel Institute (IISI); the World Capacity and Production Report, Crude Steel, Annual by James F. King; Metal Bulletin’s Iron and Steelworks of the World; and the statistical data published by such organizations as British Iron and Steel Federation (BISF), Instituto Brasileiro de Siderurgia (IBS), Japan Iron and Steel Federation (JISF), Korea Iron and Steel Association (KOSA), and Statistisches Bundesamt.

Analysis: During the twentieth century, the world steel industry increased its production of crude steel some 30 fold, from 28 million tons in 1900 to 847 million tons in the year 2000 (tonnages are metric tons). As steel became civilization’s foremost and most basic material, its output growth mirrored and made possible the building of basic infrastructure and the growth of other basic, heavy industries, thereby driving world economic and industrial development in what truly was the “Steel Century.”

In 1900, when electricity use still was very limited and the automobile was widely regarded as a dare-devil’s device, steel was made in only 12 countries, and just four - the United States, Germany, the United Kingdom, and Russia - produced 88% of all the world’s steel. By 1950, after the turmoil of economic depression and two world wars, 32 countries were in the steel business, their output totaling 190 million tons, and the United States had solidified its position as industry leader, producing 88 million tons, or a dominant output share of 46%. The next largest steel industries were located in the USSR and the United Kingdom , which produced 30 million and 18 million tons, respectively, while much of Germany ’s steel capacity had been destroyed during World War II.

Over the next two decades, yearly world steel production increased more than three fold, and the geographic structure of the industry was dramatically transformed. World output in 1970 totaled 595 million tons, with the United States accounting for 119 million tons, or a much lower 20% share. Although the U.S. steel industry had expanded its capacity, primarily in the 1950’s, steelmakers elsewhere had expanded at a much faster and more sustained pace. The Soviet Union had grown its output to 116 million tons, and strong recoveries had taken hold in the once war-ravaged industries of West Germany and most notably Japan . The latter realized a great surge in steel output from less than five million tons in 1950 to 93 million tons in 1970.

Japan ’s success in building one of the world’s largest steel industries, despite a near total lack of indigenous raw materials, including iron ore and coking coal, was made possible by using large bulk-cargo carriers to supply seacoast plants at deepwater ports. The bulk carriers revolutionized ocean transport starting in the 1950’s and negated the economic law of comparative advantage that once required integrated steel capacity to be located in close proximity to deposits of essential raw materials. This development coincided with the discovery of high-grade iron ore in Latin America, Africa, Australia, and the Far East, contributing to a shift of steel output into developing world regions and more than doubling the number of steel-producing nations to 69 in 1970 from the aforementioned 32 twenty years earlier.

For much of the world steel industry, the 1970’s were a period of boom and bust. In a single year, 1973, world output rose an unprecedented 11% or 68 million tons to 698 million tons, testing the limits of capacity in a number of countries before peaking at 709 million tons in 1974. But the seeds of collapse were sown in the midst of the boom. Steel consumers, worried about shortages, grossly overbuilt their inventories, and in late 1973, the Organization of Petroleum Exporting Countries (OPEC) increased oil prices four fold, leading to declines in world auto output, construction, and spending for capital goods.

The end of the boom came abruptly in 1975, when production dropped 9% to 644 million tons, setting the stage for a further reshaping of the world-steel map over the rest of the decade. Output declines were much more severe in some countries than in others, and some steel industries were affected very little or not at all. The United States , the European Community (EEC), and Japan saw output cuts in 1975 of 20%, 19%, and 15%, respectively, even as steel production in the communist countries and Latin America continued to increase. During the post-boom years, many steel producers in the industrialized world reduced their capacities, while their developing-world counterparts continued on a course of ambitious steel expansion.

World steel output in 1980 totaled 716 million tons, with much of its recovery after 1975 attributable to developing countries, which had increased their combined output 68%, from 60 million to 101 million tons. By 1980, significant gains in capacity and production had been made in most of the developing world, particularly in China, Brazil , and the Republic of Korea , and the number of steel-producing countries had increased to 84. Meanwhile, the United States, which was then removing capacity, had seen its share of world output decline to 14%.

Trends in world capacity and production during 1980-2000 mainly reflected the continuing growth and maturation of developing-world steel industries and the demise of the Soviet Union , which added newly independent nations to the ranks of the world’s steel producers. By the year 2000, steel was made in 90 countries, and t he world’s output that year reached 847 million tons, on track to pass a billion tons four years later. Production at the turn of the century was 131 million tons above the 1980 level, with most of the gain accounted for by just two countries, China and Korea , which boosted their combined steel output by 124 million tons.

China’s steel output, which was less than 700 thousand tons in 1950, had climbed to 37 million tons in 1980, before forging above the 100-million-ton mark in 1996, when China became the world’s number-one producer. In 2000, China melted 127 million tons, followed by Japan at 106 million, the United States at 102 million, and Russia at 59 million tons. Rounding out the production leaders were Germany and Korea , with 46 million and 43 million tons, respectively.

One of the most remarkable concluding chapters of the “Steel Century” was contributed by the Korean steel industry. During the century’s final three decades, what had been a largely agrarian country, which produced one ton of steel in 1953 and less than 500 thousand tons in 1970, drove its industrialization by building one of the world’s most modern and successful steel industries. The Korean initiative confirms that steel’s ability to transform economies remains intact, even after 100 years.

Coking Coal

Information in the Archive’s 26 coking-coal files pertains to the reserve base of coking coal, its supply and demand, its mining, production, world markets and trade, markets in the United States and Japan, coking-coal substitutes, and the use of low-volatile coal. Additional coking-coal information from the Archive’s book and reference collection is contained in such studies as World Coal Outlook: A Reassessment by Vincent J. Calarco, Jr.; three studies, Coal Trade and Transport to 1985, Future Supplies of Coking Coal, and The Outlook for Iron Ore, Cokeable Coal and Scrap, published by the Committee on Raw Materials of the International Iron and Steel Institute (IISI); the Keystone Coal Industry Manual; and The Reserve Base of U.S. Coals by Sulfur Content, The Eastern States by Robert D. Thomson and Harold York of the U.S. Bureau of Mines.

Analysis: Coking coal is the principal of two types of what are called metallurgical coals to reflect their role in producing blast-furnace iron. The other type is non-coking coal used for its heat value and directly introduced into the blast furnace by means of pulverized coal injection (PCI). Coking coal, as the name implies, is converted into metallurgical or blast-furnace coke, formed by heating the coal in coke ovens at very high temperatures and in the absence of air. The coke then is used in the blast furnace to provide heat, carbon, and burden support in smelting iron.

All large blast furnaces need coke to produce iron, while some also use PCI to reduce their coke requirements. PCI was developed and first used by Armco Steel in the early 1960’s, but was not applied on a wider commercial scale until the 1990’s in responding to restrictions on coke production. Although PCI can displace 35% or more of a blast furnace’s coke needs, tuyere-injected coal does not contribute to sustaining the furnace burden, and so the remaining coke must be stronger to maintain adequate burden support.

In 2000, world coke production totaled some 340 million tons, about 290 million tons of which was consumed by the steel industry. Some 25 million tons was used in the industry’s sinter plants and 265 million tons in its blast furnaces to smelt 577 million tons of iron, most of which then was used in making 847 million tons of crude steel. With about 1.4 tons of coal required to make one ton of coke, the world’s need for coking coal in 2000 was an estimated 475 million tons.

The selection of high-quality coking coal is the foremost determinant of coke quality in terms such factors as its mean size, strength after reaction, and stability, which make the coke capable of contributing to high levels of blast-furnace productivity. Preferred coking coals from the bituminous grades are low in volatile matter and moisture content, high in fixed carbon, and low in such impurities as ash, sulfur, alkali, and phosphorus. Because no single coking coal has all the properties blast-furnace operators prefer, blends of coking coals from multiple sources are most commonly used.

Today’s reserves of coking coal, particularly high-quality reserves, are limited in comparison to those of thermal coal, which is in ample supply at many locations around the world. Relatively fewer countries have high-quality coking coal, its main deposits being located in the United States , Canada , and Australia .

Companies, in U.S.

The Archive contains 280 document files on steel companies in the United States. Information in the files, some dating from the 1860’s, relates both to currently operating companies and to those no longer in existence for a variety of reasons, including corporate reorganizations, bankruptcies, sales, acquisitions, mergers, and takeovers by conglomerate corporations.

The files provide information on the following 65 companies:

- Acme Steel Co.

- Allegheny-Ludlum SteelCorp.

- A.M. Byers Co.

- American Bridge Co.

- American Sheet Steel Co.

- American Steel & Wire Co. of New Jersey

- American Steel Hoop Co.

- American Tinplate Co.

- American Rolling Mill Co.

- Atlantic Steel Co.

- BRW Steel Corp.

- Bayou Steel Corp.

- Bessemer Steamship Co.

- Bethlehem Steel Corp.

- Birmingham Steel Corp.

- Cambria Steel Co.

- Cascade Steel Rolling Mills Inc.

- Colorado Fuel & Iron Co.

- Commercial Metals Co.

- Connecticut Steel Corp.

- Continental Steel Corp.

- Copperweld Steel Co.

- Cyclops Corp.

- Detroit Steel Corp.

- Edgewater Steel Co.

- Federal Steel Co.

- Ford Steel Division

- Geneva Steel Co.

- Georgetown Steel Corp.

- Granite City Steel Co.

- Gulf States Steel Co.

- Inland Steel Co.

- Jones & Laughlin Steel Corp.

- Kaiser Steel Corp.

- LTV Corp.

- Lake Superior Consolidated Iron Mines

- Latrobe Steel Co.

- Lukens Steel Co.

- McLouth Steel Co.

- NVF/Sharon Steel Corp.

- National Enameling and Stamping Co.

- National Steel Corp.

- National Tube Co.

- New Jersey Steel Corp.

- North Star Steel Co.

- Nucor Corp.

- Oregon Steel Mills Inc.

- Phoenix Iron Co.

- Phoenix Steel Corp.

- Pittsburgh Steel Co.

- Republic Steel Corp.

- Roanoke Electric Steel Corp.

- Schnitzer Steel Industries

- Sharon Steel Co.

- Sharon Steel Hoop Co.

- Shelby Steel Tube Co. of New Jersey

- Simonds Steel Mills

- Taylor-Wharton Iron & Steel Co.

- United States Steel Corp.

- Warren Consolidated Industries

- Inc.

- Weirton Steel Co.

- Wheatland Tube Co.

- Wheeling-Pittsburgh Steel Corp.

- Wisconsin Steel Co.

- and Youngstown Sheet and Tube Co.

Information in the files varies from company to company and extends to the following major subjects: company histories, company and plant profiles, facility descriptions, visitor’s brochures, operating reports, product information, market analyses, production and shipments data, production by plant, production-cost analyses, wage and price information, financial reports, sources and uses of funds, profit-sharing agreements, private placements, partnerships, acquisitions, capital appropriations, modernization and expansion, strategic plans, facility retirements, plant closings, reorganizations, corporate correspondence, technical papers, congressional testimony, speeches, and management biographies.

Additional information on U.S. steel companies is contained in the United States sub-division of the category “countries, steel-producing,” as well as in a number of the Archive’s books and references, including its collection of steel-company Annual Reports and the AISI Iron and Steel Works Directory.

Analysis: During the twentieth century, the U. S. steel industry’s roster of active companies underwent recurring change. This was particularly the case during periods of widespread consolidation and restructuring, starting in the early 1900’s with the formation of United States Steel Corporation, next with the wave of conglomerate takeovers, mergers, and bankruptcies during the mid-1960’s through the 1970’s, and finally, with the onset of buyouts and mergers in the early 2000’s.

While consolidation was removing names from the corporate roster, the addition of new companies resulted from the construction of steel plants during World War II and, starting in the early 1960’s, from the development of minimill technology, which significantly lowered the barriers to entering the steel business and led to the formation of many new corporate entities, including Nucor Corporation, which was to become the largest producer of steel and recycler of steel scrap in the United States.

Countries, Steel-Producing

The Archive contains 1,333 document files providing information and data on the steel industries and associated industrial activities in the following 56 countries and world regions: Algeria, Argentina, Australia, Austria, Belgium-Luxembourg, Brazil, Canada, Chile, China, Denmark, ECSC, Egypt, Finland, France, Germany, Ghana, Greece, Hungary, India, Indonesia, Iran, Iraq, Ireland, Italy, Japan, Korea, Lebanon, Libya, Mexico, Mid-East, Mozambique, Netherlands, New Zealand, Nigeria, Pakistan, Philippines, Poland, Portugal, Qatar, Saudi Arabia, Serbia, South Africa, Spain, Sweden, Switzerland, Syria, Trinidad and Tobago, Taiwan, Turkey, Uganda, USSR and Russia, United Kingdom, United States, Venezuela, Vietnam, and the World.

A unique perspective on national and international steel developments over much of the last century is afforded by the document files for each country, which contain diverse information on their steel industries, as well as for individual steel companies and plants. The information, which varies in content and scope from country to country, covers a broad array of economic, corporate, commercial, financial, technical, and governmental subjects.

The major subjects covered include the following: national and regional economic conditions and data, indigenous and imported raw materials, domestic energy supplies, steel-industry statistics, steel-industry and company histories and profiles, steel-plant feasibility studies, plant profiles and visitor’s brochures, plant capacities, shipbuilding plants, plant closings, steel facility descriptions and evaluations, technology and process utilization, steel-market conditions and surveys, steel consumption per capita, product information and quality programs, production data and forecasts, production costs, labor costs and industrial relations, capital input per worker, freight costs, bulk-carriers, steel shipments and pricing, competitive conditions, steel imports and exports, trade agreements, trade association profiles, financial reports, corporate strategies, capacity expansion and replacement, profitability, capital-investment needs, sources and uses of funds, overseas financing, credit-facility memoranda, restructurings, bankruptcies, diversification, privatization, environmental reports, technical and engineering bulletins, press releases, speeches, correspondence, government steel plans, tax policies, and government regulation.

Further information on the world’s steel-producing countries is provided in the steel book and reference collection, which contains a number of corporate and industry histories; the Steel Statistical Yearbook of IISI; the annual statistical reports published in a number of countries, including Brazil, China, Germany, Japan, Korea, the United Kingdom, and the United States; steel reports prepared by the European Coal and Steel Community (ECSC), the Latin American Iron and Steel Institute (ILAFA), and the United Nations; and Metal Bulletin’s Iron and Steel Works of the World. Finally, extensive information on the steel-producing countries is contained in five of Father Hogan’s books: World Steel in the 1980’s, Global Steel in the 1990’s, Capital Investment in Steel, Steel in the 21 st Century, The Steel Industry of China , and The POSCO Strategy.

Energy

The 79 document files on the subject of energy contain papers, speeches, published articles, references, and statistics generally focused on measures taken within and outside the steel industry to address concerns and problems arising from the energy crisis of 1973-1974 and the additional surge in oil prices during 1979. A number of documents describe the energy-conservation measures taken by the steel industry, both in the United States and around the world, while other documents provide information on such subjects as the energy requirements for iron and steel production, energy-saving technologies at steel plants, power costs in the steel industry, the cost of steel-plant steam, coal-based energy, coal gasification, nuclear energy, plasma melting, and the relative energy intensities of steel and other materials. In addition, the Archive’s book and reference collection contains such works as The Oil Import Problem by Sebastian Raciti and A Technological Study on Energy in the Steel Industry by the Committee on Technology of IISI.

Environment

Particularly after the mid-1960’s, the world steel industry increasingly shaped its investment and operating decisions to reflect a growing environmental concern and the need to attain compliance with increasingly stringent pollution-control standards. The Archive’s 69 document files on the environment examine industry measures to abate the air and water pollution associated with such activities as mining iron ore, making coke, producing iron and steel, and rolling and processing finished steel products. In addition, the documents assess the economic impact on the industry and review the technologies and operating changes involved in making steel plants more environmentally compatible. The contents of the files include consultants’ studies prepared for AISI, Reserve Mining Company, and the U.S. Environmental Protection Agency (EPA), as well as papers and studies by AISI, IISI, and a number of steel companies. In addition, Steel Production: Processes, Products and Residuals by Clifford S. Russell and William J. Vaughan is included in the Archive’s book collection.

Analysis: Energy and the environment are interrelated subjects, since the most effective way to avoid environmental pollution is to reduce energy consumption. During the past three decades, the energy consumed in steelmaking has been cut by more than 45%, limiting carbon dioxide emissions by a comparable amount. At the same time, air and water pollution from steel mills has been reduced by upwards of 90%. Contributing to this progress has been the application of the latest in control technologies and savings in energy that have resulted from the adoption of such production advances as continuous casting, direct rolling, waste heat recycling and cogeneration, and the use of more recycled ferrous scrap, mainly in electric-arc furnaces, and also as a result of process and practice changes in the basic-oxygen furnace or BOF.

Not only is steel the most recycled production material, but in the form of ferrous scrap that has been melted previously, it stores energy and can be reused over and over again. The steel industry puts some recycled steel into virtually all the new steel it produces, and by emphasizing recycling, it conserves both energy and such raw materials as iron ore and coking coal, which limits both land disturbance and greenhouse-gas emissions. Underscoring the extent of the industry’s recycling effort, some 98% of all cars are now recycled, and 28% of all the steel in the UltraLight Steel Auto Body (ULSAB) is made from recycled ferrous scrap.

During 1990-2002, the U.S. steel industry’s energy intensity per ton of steel shipped declined 17% to some 14 million BTU’s, and the industry has made a commitment to achieve an additional 10% reduction by 2012, which will require continuing investments in new technologies to both increase productivity and further reduce carbon dioxide and other emissions.

Iron Ore

The Archive’s 144 files on iron ore provide information on such subjects as world supply and demand, market analyses, iron-ore economics, production statistics, iron-ore trade, ore prices, world and country reserves, captive supplies, costs of production and shipping, bulk-carrier ore transport, beneficiation, pelletizing, sintering, world pellet-plant capacity, taconite production, mining-project profiles, mining-company histories and financial reports, and iron ores from Australia, Brazil, Canada, Liberia, Mexico, Sweden, the United States, and Venezuela. This information, including iron-ore research by Thomas E. McGinty, is complemented by a number of the Archive’s books and references, such as the statistical report, Iron Ore, published annually by the American Iron Ore Association (AIOA); the study Iron Ores and Ironmaking in the World by Battelle Memorial Institute; the BHP Pocketbook of the Broken Hill Proprietary Co. Ltd.; An Inventory of the Free World’s Iron Ore Deposits, an unpublished study by F.M. Chace; The Changing World Market for Iron Ore, 1950-1980 by Gerald Manners; the Cliffs Iron Ore Analyses, published annually by Cleveland-Cliffs Inc.; Metal Bulletin’s Iron Ore Databook; three studies by the IISI Committee on Raw Materials, Report on Iron Ore, Past Trends, 1950 to 1974, The World Market for Iron Ore, and The Outlook for Iron Ore, Cokeable Coal and Scrap; the Iron Ore Analyses of Malmexport AB; the United Nations’ publication, Survey of World Iron Ore Reserves; and the Proceedings of the Ninth Pacific Trade and Development Conference on Mineral Resources in the Pacific Area.

Analysis: In 2000, the world produced 1.07 billion tons of iron ore, used mainly to supply blast furnaces smelting 577 million tons of iron. The leading ore producer was China, which mined 224 million tons of mainly low-grade ore with an average iron content of about 30%, less than half the content of China’s imported ores. Much of the domestic ore must be enriched using concentrators installed at a number of mines. By contrast, the world’s second and third largest producers, Brazil and Australia , mine ores containing 65% or more iron, their 2000 outputs amounting to 209 million and 168 million tons, respectively. Next in line among the world’s top ore producers were Russia with 87 million tons, India with 73 million, and the United States with 63 million tons.

Fortunate for the world steel industry, iron-ore resources are in abundance, being located beneath 4% to 5% of the earth’s crust. They are not, however, distributed evenly, with large, rich deposits found in some countries and virtually none in others. Japan , for example, despite its 2000 ranking as the world’s second largest steel producer, relies on imports for all of its ore, while Brazil , number eight in steel, has enough rich ore reserves to supply the entire world for at least the next 25 years.

Much of the ore now used by the world’s iron and steel producers is beneficiated or upgraded to some extent, the two most common upgrading methods being sintering and pelletizing. Sinter is produced by heating fine ore mixed with coal dust or coke breeze to obtain a clinker-like substance, whereas iron-ore pellets, which usually are less than one inch in diameter, are made from concentrates of varying qualities of ore, including taconite. Both upgraded ore products make the blast-furnace burden more permeable, which contributes to furnace productivity.

Labor

The 27 labor files provide information on steel-industry labor relations, primarily in the United States, treating such subjects as historical developments dating from the 1850’s, labor costs and productivity, collective bargaining, labor disputes and strikes, labor agreements, pensions and pension liabilities, wage stabilization, and supplemental unemployment benefits. Also included are a number of files dealing with the guaranteed annual wage, a subject studied extensively by Father Hogan, who in 1953 became a member of United States Steel’s Guaranteed Wage Subcommittee. Additional information on steel labor is provided in the files on individual-country steel industries under the heading “industrial relations,” and in the Archive’s books and references, including Current Practices in Industrial Relations in the Steel Industry by the Committee on Industrial Relations of IISI, The Steel Workers by John A. Fitch, Labor Policy of United States Steel Corporation by Charles A. Gulick, Collective Bargaining in the Basic Steel Industry by the U.S. Department of Labor, John L. Lewis by the United Mine Workers of America, and Father Hogan’s books Productivity in the Blast-Furnace and Open-Hearth Segments of the Steel Industry and Economic History of the Iron and Steel Industry in the United States (Five Volumes).

Analysis: During 1980-2003, despite a 35% increase in world crude steel production from 716 million to 965 million tons, steel-industry employment underwent sharp declines in most countries. An average decline of 57% was experienced in 24 countries for which IISI tracks data, all of which saw steel employment trend significantly lower over the period. In the European Union, it fell 66%, from 792 thousand to 269 thousand workers. In the United States and Canada , it fell 61%, from 460 thousand to 179 thousand, and in Japan from 380 thousand to 170 thousand workers, a decline of 55%. Likewise in Brazil , steel employment dropped 48%, from 132 thousand to 68 thousand workers. With steel production and industry employment trending in opposite directions, the production of each worker rose some 200% in the EU, about 140% in the United States and Canada, and approximately 115% in Japan.

These marked gains in worker production and the associated declines in steel employment can be traced to a number of world-steel developments in the post-1980 period. Heightened domestic and international competition within the steel industry, including the competitive challenge from minimills, has combined with external competition from substitute materials to make continual cost reduction imperative to steel-company survival. To lower their costs, steel companies in both industrialized and less-developed countries have rationalized, privatized, and consolidated their capacities, sometimes internationally, thereby eliminating redundant operations. At the same time, the ongoing transition from batch-type to more efficient, continuous processing in the manufacture of steel has eliminated multiple production steps and their onetime labor requirements.

Markets, Steel

Information on the markets for steel, often called the steel-consuming industries, is provided in 247 document files relating to steel-product usage in agriculture, appliances, automobiles, construction, general applications, the oil and gas industry, the railroad industry, and shipbuilding. Other, broad-based market information and data are contained in Father Hogan’s five-volume economic history of steel, in the Archive’s collection of statistical reports for various countries, and in such books and references as Large Uses in Small Ways, the AISI publications Steel Facts and Charting Steel’s Progress, the Organization for Economic Cooperation and Development (OECD) publication The Steel Market in…and Outlook for in various years, and the Economic Commission for Europe (ECE) of the United Nations publication The Steel Market in for various years. The historical and other steel-market developments recounted below, which are primarily based on the U.S. experience, reveal the interdependence of the steel industry and other industries that are consumers of iron and steel products.

Agriculture

The files relating to steel’s contribution to agriculture include documents on the farm-equipment industry, Deere and Company, International Harvester Company, various types of farm machinery and equipment, tractor sales by end use, tractor prices, and census data on farms and farm equipment.

Analysis: The agricultural revolution of the twentieth century is a tribute to generations of farmers and ranchers, who by their hard work have harnessed a recurring stream of scientific and mechanical innovation to greatly improve soil preparation and conservation; the planting, cultivation, harvesting, and rotation of crops; and the breeding and raising of livestock. Compared to 1900, when each farmer was able to supply enough food and fiber to sustain eight persons, a remarkable growth in farm productivity pushed that number to more than 200 as the century drew to a close. The mechanization of agriculture was one of the prime movers of this progress and never would have been possible without the use of iron and steel.

The contribution of iron and steel to agriculture has come with the development of a wide variety of farm machinery and equipment. Starting in the early 1800’s, iron first replaced wood in the manufacture of horse-drawn plows, and in 1846, an Illinois blacksmith named John Deere rolled the first cast steel for plows. By the mid-1800’s, the machine age of farming had dawned, when Cyrus McCormick’s reaper, incorporating iron and steel parts made from bars, plates, and rods, reduced the cost of harvesting by one-third, and threshing machines had come into widespread use in large grain fields.

Nonetheless, through the first two decades of the twentieth century, wire and posts for fencing continued to represented the principal market for steel on the farm, a far more essential role awaiting the 1920’s, when the introduction of gasoline-powered tractors needing steel in significant quantities seriously started to displace horses in favor of mechanized plows. On U.S. farms, the use of draft animals had reached its peak in 1918, when the farm population of horses and mules totaled 26.7 million, compared to only 85 thousand tractors, many of which were big and inefficient, steam-powered units.

It also was in 1918, immediately after World War I, that Ford Motor Company gave mechanized farming a major boost by mass-producing 34 thousand gasoline-powered Fordson tractors. Soon the tractor became a source of energy to operate such power-driven machines as mowers, corn pickers, harvesters, and combines, and once farmers rapidly adopted the internal combustion engine, steel’s role in agriculture became indispensable.

Today, following decades of improving farm productivity, crop yields are benefiting from global positioning system (GPS) technology that enables the farmer to plow perfectly straight rows from the air-conditioned cab of a satellite-guided tractor, which continues to be made mainly of steel.

Appliances

The Archive’s files on steel use in appliance manufacturing provide information on the history of steel in appliances, electrical-appliance sales, the use of appliances in U.S. homes, and steel shipments to the appliance industry.

Analysis: As the twentieth century dawned, relatively small amounts of iron and steel were being used to make stoves, kitchen utensils, and cutlery, and some 25 years were to elapse until three major developments gave rise to an appliance industry that was to become a thriving new market for steel. First, households and other consumers started to replace their old cast-iron stoves with sheet-steel kitchen ranges. Second, manufacturers of washing machines started to turn away from wood and copper in favor of galvanized steel. And third, manufacturers of household refrigerators, which had first been introduced in 1912, started to overcome consumer resistance with more reliable electric models, which became an acceptable alternative to the old-fashioned, wooden icebox. With these trends in place, appliance makers started to develop closer working relationships with the steel industry.

Like the icebox, the first refrigerators also were made of wood, which was subject to rot, a problem overcome in 1927, when General Electric Company introduced the all-steel refrigerator. Beyond the major appliances, steel also became the preferred material for manufacturing a variety of smaller household appliances, such as vacuum cleaners, electric irons, water heaters, toasters, hot plates, waffle irons, and other small cooking implements. So popular did new appliances of all types become that their sales and consumption of steel increased even during the Great Depression, with the exception of only two years, 1932 and 1938.

During World War II, appliance manufacturing was largely suspended, and after the war, the appliance industry ramped up its output to meet pent-up demand, introduced refinements and new features to its existing product line, and then started to market a number of new products, including clothes dryers, freezers, dishwashers, and room air conditioners, all of which were and continue to be built primarily from steel.

Automotive

The document files contain information about the development of this leading steel market, including automobile-industry and company histories, the production of automotive steels, growth of the auto-steel market, the location of U.S. auto plants, the auto industries of Japan and Korea, world auto-industry relationships and surveys, auto-industry economics and competition, industry capital expenditures, auto-company sales and profits, partnerships between the steel and auto industries, competition from substitute materials, plastics and auto recycling, automotive use of Zincrometal, statistical references and research, motor-vehicle statistics of Japan, statistics on trucking, trucks vs. freight trains, the Titus mill and the automobile body, early automobiles, the Selden Patent, automobile mass production, the Chrysler and American Motors merger, interviews with Charles S. Mott of General Motors and Edward Fisher of Fisher Body, automobile and truck brochures, and publications of the Automobile Manufacturers Association (AMA) and General Motors Corporation. In addition, the AMA publication Automobile Facts and the IISI report Intermaterial Competition for the Body in White of the Passenger Car are contained in the Archive’s reference collection.

Analysis: In 1900, there was such fear surrounding the first automobiles that a Vermont ordinance required a mature person waving a red flag to walk one-eighth of a mile in front of any moving vehicle. For the steel industry, automobile builders scarcely existed as a market, and except for engine production, wood was practically the universal automotive material, not only for the body, but for wheels and axles as well. The sheet and alloy steels that one day would be widely used by the auto industry were produced only in limited quantities.

During 1900-1920, all of this started to change. The hundreds of small car-building shops of the 1890’s gave way to fewer, more entrepreneurial companies with innovative leaders, who eventually transformed the automobile from an expensive horseless carriage into a more reliable and affordable mode of transportation. Leaders named Benz, Buick, Durant, Ford, Leland, and Olds did this by adopting the basic principles of mass production, including the assembly line, standardized and interchangeable parts, and efficient plant and equipment layouts, all manufacturing methods they appropriated from the meat-packing, firearms, and machine-tool industries and then brought to new levels of refinement and perfection.

As automobiles started to win broader acceptance, the steel industry and other suppliers strove to meet the auto industry’s special needs. States and localities started to build paved roadways, which were practically non-existent. Gasoline was made more plentiful by advances in the cracking process for petroleum, and the rubber industry worked to develop smoother-riding, more wear resistant tires. One by one, limitations on the auto industry’s growth started to be eliminated.

At first, automakers pretty much took their steel as they found it, using steels produced for other purposes. Gears were cut from tool steel, and engine parts were made from billets intended for rolling rails. Tubing for bicycles was used in building chassis, and cylinders were cast from iron suited for stoves. All of this made for vehicles that were constantly breaking down, and by 1905, auto engineers, notably those at Ford Motor Company, had identified the need for automotive steels with particular properties. Before long, the interdependence of the steel and automobile industries was to become well established.

By 1910, the development of alloy steels made to automakers’ specifications was proceeding rapidly, and the Society of Automotive Engineers (SAE) went to work in establishing a standard specification system to classify steels by alloy content. Up to that time, the preoccupation of automakers with mechanical problems saw most auto-body design and construction farmed out to builders of coaches and buggies. Accustomed to working with wood, they first used steel panels attached to wooden frames only because finishing the steel took one-third less paint than did wood sheathing. The early bodies they designed were a mass of straight lines and right-angle bends, so that steel sheets without drawing qualities, similar to black plate for tinning, were adequate for their needs.

After 1910, angular automobile designs started to be discarded in favor of more contoured models, a trend that called for the development of forming dies, stamping presses, and above all, higher grade, drawing-quality steel sheets. Auto companies began to specify sheets having particular formability and surface qualities, and the steel industry worked to meet these demands by improved box annealing and by supplying unprecedented quantities of hand-rolled, full-finished sheets for the stamping of hoods, hood sides, and fenders.

By 1920, although the railroad industry remained the principal market for steel, the auto industry had become one of the fastest growing sources of steel demand. That year, U.S. automakers consumed 915 thousand tons of rolled, finished-steel products, up from only 71 thousand tons ten years earlier. This increase in the auto-steel market reflected the growth of car and truck production from 187 thousand to 2.2 million units.

Industrial growth during 1920-1930 was spearheaded by the automobile industry, which continued to place demands on its supplier industries for ever-increasing quantities and qualities of their diverse products. Among the important factors driving the auto industry’s growth were a shift from the open to the closed car, lower car prices, lower operating and repair costs, credit and installment buying, and a four-fold expansion in the miles of paved roads and highways.

The shift to the closed car and the introduction of the monopiece body by the Budd Company brought radical changes in stamping requirements and placed demands on the steel industry for much wider, hand-rolled sheets. However, beyond upgrading their hand-rolling operations, steel producers were to respond to burgeoning sheet demand by adopting one of the all-time, most significant advances in steel technology, the continuous hot-strip mill. In January, 1924, the American Rolling Mill Company placed into operation at its Ashland , Kentucky plant the first successful continuous wide strip mill, which by 1927 was rolling 36 thousand tons a month, twice the level needed to make the mill pay. By the mid-1930’s, the U.S. steel industry was to invest half a billion dollars to install 27 such mills with a combined annual rolling capacity of nearly 13 million tons.

The auto industry was to be the principal steel consumer served by this new capacity. However, the auto market’s growth was interrupted by the Depression, followed by the suspension of civilian auto output in mobilizing for World War II. In 1929, the industry sold 5.3 million vehicles, a record that would stand until 1949. Automotive steel consumption in 1929 reached 5.5 million tons, marking a five-fold increase in under ten years. But this tonnage wouldn’t be regained until 1936-37, and at the depths of the Depression in 1932, auto output dropped to 1.3 million units, the lowest level since 1918.

Rather than slowing automotive progress, the weak auto market of the 1930’s heightened competition and gave rise to major design changes, aimed at adding sales appeal to cars of the day. Such innovations as the all-steel body, the turret-top, and streamlining, not only increased the steel content of the average car, but also called for the development of more advanced drawing-quality sheets with metallurgical properties capable of withstanding the radical stamping impressions needed to execute the new designs. The steel industry was quick to respond to this requirement, given extremely depressed overall steel demand and the fact that the auto industry, having displaced the railroads to become the leading tonnage consumer of steel in 1931, was by then firmly established as the most important steel market in revenue terms as well.

In 1948-49, as automakers worked to keep pace with pent-up demand after World War II, U.S. car and truck output once again climbed above the five-million-unit level, last exceeded 20 years earlier. However, given the significant design changes favoring steel, many of which had been initiated in the 1930’s, each post-war motor vehicle contained an average 75% more steel, boosting the auto industry’s yearly steel consumption toward 10 million tons for the first time.

In 1950, when world motor vehicle production was approximately 10 million units, North American automakers accounted for an output share of more than 80%. Over the next fifty years, world production trended upward to 58 million units in 2000, and the North American output share declined to some 25%, with roughly equivalent shares accounted for by Europe , Japan , and all other nations. This growth and geographic dispersion of car and truck production made the automobile industry a major, if not the leading, source of steel demand in many countries, including the United States, Canada, Brazil, Japan, Korea, the United Kingdom, Germany, France, Italy, and Spain.

By the late 1950’s, an active international trade in motor vehicles and parts started to emerge, with the United States becoming the major import market for Volkswagen Beetles and Toyotas. Since then, the world auto trade has become a $500-billion-plus annual business, increasing international competition, most notably in the United States, Europe, and Japan, as well as international auto-company ownership, joint ventures, and the establishment of so-called transplant manufacturing facilities. In addition to becoming increasingly international, the world auto industry has undergone other major changes that have influenced its role as the steel industry’s most important market. In the late 1960’s, growing concerns for the environment and automotive safety started to bring about revolutionary advances in automotive design and engine technology that have continued to the present.

In the 1970’s, OPEC’s two major oil shocks set in motion programs to downsize U.S. cars and to reduce the weight of vehicles everywhere in the interest of increased fuel efficiency. This led to increased materials competition from lighter substitutes, including plastics and aluminum, and also to ongoing innovations by the steel industry, including the development of light-weight-high-strength steel sheets, high-tech galvanizing and other corrosion-resistant sheet coatings, and the manufacture of tailor-welded blanks or semi-parts for auto-body construction.

The many challenges faced by the automobile and steel industries have forged an even closer working relationship between them, typified by the Auto/Steel Partnership Program, which involves both industries in nearly every phase of automotive design. The result has been to convert all high-volume vehicles to weight-saving monologue construction in which the steel body itself accounts for the vehicle’s styling, structural integrity, and crash-energy management. Such auto-steel advances have enabled automakers to fulfill their obligations to the environment, fuel economy, and passenger safety, while continuing to meet the market’s needs for a wide variety of vehicles, from sedans and coupes, to minivans and sports-utility vehicles (SUVs). Now, as automakers look to build tomorrow’s hybrid- and hydrogen-powered cars, their close interdependence with the steel industry insures their continuing role as the largest and most important steel market.

Construction

The Archive’s files on the construction market for steel provide information on modern steel construction, steel and architecture, structural steel, construction plates, steel and wood for residential construction, steel for bridges, steel for infrastructure building, construction alloy steels, “Cyclone” steel fencing, history of the structural mill, history of Otis Elevator Company, history of the skyscraper, early iron construction, the market for structural steel in New York City, expansion of the George Washington Bridge, outlook for the housing industry, U.S. steel shipments to the construction industry, an address by James B. Eads of Eads Bridge fame, and publications and papers on steel construction from the American Institute for Steel Construction (AISC), AISI, IISI, and United States Steel Corporation. Additional information on steel and construction is contained in the Archive’s book and reference collection in the following: A.I.S.C. Structural Shop Drafting Textbook, and Steel Construction – A Manual for Architects, Engineers and Fabricators of Buildings and Other Structures, both published by AISC; Iron and Steel Beams, 1873 to 1952, edited by Herbert W. Ferris; and David McCullough’s The Great Bridge.

Analysis: Construction activity, second to auto manufacturing as the largest source of steel demand, encompasses a multitude of diverse project types, from public works, such as highways, bridges, tunnels, airports, dams, and wastewater treatment plants; to commercial construction, including manufacturing plants, warehouses, retail outlets, and office buildings; to residential construction, encompassing single- and multiple-family homes and apartment buildings. The most steel is consumed in the heaviest projects, most of which are most often classified under the general heading of infrastructure and are often designed to provide some basic service to the general population.

The building and improvement of infrastructure represents a recurring need in both industrialized and developing countries, generating an ever present, though fluctuating market for such steel products as structural shapes, plates, concrete reinforcing bars, wire, and pipe. The extent of infrastructure building at any given time is usually determined by the availability and allocation of public funding, and many industrialized countries in recent years have placed a higher priority on social spending, which has created backlogs of delayed infrastructure projects.

Reinforced concrete has been the principal competitor of steel in infrastructure building and for other heavy construction projects, challenging steel even in high-rise construction. In recent years, however, the market inroads made by concrete appear to have been stabilized, and steel has been mounting an effective competitive challenge of its own, most notably against wood in framing for residential construction.

The steel industry had attempted to introduce steel-framed homes as early as 1933, with an exhibition at the Chicago World’s Fair, but its effort did not meet with significant market success until some six decades later, when a sharp escalation of lumber prices started to erode the resistance of carpenters and builders accustomed to working with wood. The use of galvanized steel framing has since made significant inroads into the home-building market, assisted by an active educational and sales promotion effort by steel companies and their trade associations, including AISI and IISI. Meanwhile, galvanized steel has become the preferred framing material for use in constructing hospitals, office buildings, shopping malls, and other commercial buildings.

General

The “General” files contain documents on the overall steel market and also on more specific sources of steel demand not categorized elsewhere in the Archive. The information provided includes steel-market forecasts, economic forecasts, instructions for reporting steel shipments, steel consumption by industries, steel distribution to consuming groups, demand for merchant wire products, capital-goods expenditures, high-technology capital spending, steel use in the electric-machinery industry, steel use in the chemical industry, and the U.S. geographic markets for tinplate.

Oil and Gas

Files on the oil and gas industry as a market for steel provide information on the nature of the industry, its competitive structure, its worldwide capital investments, their effect on the steel market, petroleum company financial analyses, world oil-country-tubular-goods (OCTG) mills, the OCTG market, U.S. statistical data on OCTG, world OCTG shipments, oil and the environment, and steel for offshore drilling in the Gulf of Mexico.

Analysis: Underscoring industrial interdependence, a steadily increasing U.S. automobile population in the 1920’s pushed gasoline demand and crude oil production to record levels. The gasoline that fueled the auto industry’s success required increased crude oil production and advances in the cracking process first introduced in 1913 by Standard Oil of Indiana, which had doubled the yield of gasoline from crude to 20%. During the 1920’s, oil output rose from 440 million to one billion barrels, and with gasoline yields improving to more than 40%, gasoline production increased to 435 million barrels.

By about 1925, exploratory drilling already had been carried out at most U.S. locations with surface indications of possible oil or with favorable domed land formations, like the one that led to the famed 1901 strike at Spindle Top in Texas . Thereafter, the science of geology, once spurned by many oil companies, came into wider use, along with the first portable seismographs, to help locate domes in the sub-strata.

More recently, to meet the world’s growing oil and gas needs, oil explorers and geologists have been locating new reservoirs by using three-dimensional seismic technology teamed with powerful computers to turn voluminous sonic and acoustic measurements into sophisticated maps and high-resolution images, affording them detailed views of geological formations many miles below the earth’s surface, whether land or sea. While Spindle Top’s oil was a thousand feet down, today’s wells are commonly drilled to 15 thousand feet or more. Even at increasing depths, however, new technology promises to improve the success rate of exploratory wells from 30% to some 50% in the years ahead.

The deeper the exploratory or production well to be drilled, the more steel is needed in the form of drill pipe, oil-well casing, and tubing. A well 15 thousand feet deep requires about 55 tons of OCTG, with additional steel plates and structural shapes needed to build a drilling platform and a 15-story drilling rig. But this is just the beginning. Substantial quantities of steel also are needed to collect the crude oil or natural gas, to build and maintain refinery capacity, to move the gas, oil, and refined oil products by pipeline to distant markets, and to construct storage and distribution facilities.

In a continuing effort to reduce drilling costs and maximize production from new and established reservoirs, the oil and gas industry has been adopting a number of innovative drilling technologies. These have included the horizontal production well, which laterally penetrates a reservoir and circumvents the need to drill additional vertical wells; the multilateral well, which is drilled from an established well, which is then closed off; and the designer well, drilled with precise targeting and often redirected to tap multiple pockets of oil within a given reservoir. Although these innovations can reduce the steel consumed in drilling, the oil and gas industry would be unable to function without steel, as would the automobile industry that makes cars and trucks so dependent on oil and gasoline.

Railroads

Document files on the railroad industry and its role as a steel market contain information on the early history of U.S. rail production, chronological and historical facts on the railroad industry, railroad company histories, railroad statistics, railroad steel demand, steel for rail and rail-car production, locomotive building, diesel vs. electric locomotives, box and refrigerator cars, piggy-back flat cars, railroad operations and costs, railroad capital expenditures, administered rail rates and competition, and papers and publications of the Association of American Railroads (AAR) and locomotive builders General Electric Company and Westinghouse Electric Corporation. The Archive’s reference collection includes such AAR publications as A Review of Railroad Operations, Railroad Review and Outlook, and Yearbook of Railroad Facts.

Analysis: Dating from the 1870’s, the U.S. steel industry’s early growth and development was closely tied to the manufacture of rails for an expanding railway system, which by 1930 operated 430 thousand miles of track. Then, as the Depression brought severe declines in railroad operations, the automobile industry displaced the railroads as the leading steel market. In 1932, U.S. rail production fell below a million tons for the first time in over 50 years, and the production of rolling stock slowed to a crawl. The result was to cut the railroad industry’s share of total finished steel demand to 10% from more than 25% ten years earlier.

During the 1950’s, the railroad industry in many countries started to see its dominant position in passenger and freight transportation increasingly challenged by the trucking and airline industries, gradually diminishing its role as a steel consumer. This threatened to make the market for railroad steels a replacement market, related primarily to maintaining the rails, rolling stock, and infrastructure of existing railroads and commuter rail systems. However, over the last few decades, railroads have moved to counter their losses in passenger traffic by constructing new, high-speed railways, thereby giving renewed impetus to their role as steel consumers. The high-speed trains, which are capable of traveling in the range of 125-200 mph or faster, have created a demand for rails and for other steel products needed to build new rights of way and to manufacture more powerful locomotives and sleek new passenger cars for the railways of tomorrow.

Shipbuilding

Documents in the shipbuilding files contain information on the shipbuilding industry’s history, industry profiles and statistics, new ship construction, ports and ore carriers, the optimum size of ore carriers, the U.S. bulk-carrier fleet, and a brief history of the U.S. Merchant Marine. In addition, the book and reference collection includes Big Load Afloat: U.S. Domestic Water Transportation Resources by the American Waterways Operators and the IISI publication The Seaborne Transport of Iron and Steelmaking Raw Materials.

Analysis: The shipbuilding industry is a significant steel consumer in a number of countries, although the industry’s business and its steel needs have been very cyclical. During 1975-2000, for example, the world’s annual deliveries of ships over 100 gross tons varied from a 1975 peak of 34.2 million gross tons to a 1988 low of 11.3MGT, followed by an irregular recovery to 31.7MGT at the end of the period.

Most of the industry’s ship tonnage is accounted for by very large vessels, including oil tankers, which in recent years have provided about 23% of the total, freight and container ships (20%), chemical tankers (14%), bulk-cargo carriers (14%), and cruise ships (9%), with the remaining one-fifth of the business in the form of LNG carriers, offshore oil platforms, naval vessels, and other ships. Their construction requires a number of specialized steel products, including various grades and sizes of shipbuilding plates, bulb flats, pipe and fittings, and special shapes and profiles. Among the plate products consumed are anti-corrosion grades for crude-oil tankers and clad and stainless grades for chemical tankers.

Among the very large ships, tankers are built at yards in Brazil, China, Croatia, Japan, Korea, Poland and the United States; container ships in China, Denmark, Japan, Korea, Poland, and Taiwan; bulk-cargo carriers in China, Japan, Korea, and Taiwan; LNG carriers in Japan, Korea, and Spain; and cruise ships in Finland, France, Italy, and Japan.

Far and away, the world’s number-one shipbuilding region is the Far East , which accounted for nearly 84% of total tonnage deliveries in 2000, up from 51% in 1975. In 2000, Korea became the world’s leading shipbuilder on a tonnage basis, delivering 12.2MGT and moving slightly ahead of Japan , which delivered 12.0MGT. Ranking third in the world was China at 1.6MGT. Among other regions, Western Europe contributed about 11% of the world’s ship tonnage, Eastern Europe about 4%, North and South America less than 1%, and all other countries some 2%.

Starting in the 1950’s, when bulk cargo carriers of 50 thousand DWT were considered large, Japan’s steel and shipbuilding industries spearheaded the growth of bulk-carrier size to accommodate the transportation needs of the country’s rapidly expanding, deepwater steel plants. Notably, both of today’s dominant shipbuilding countries, Korea and Japan, have major, coastal steel plants with a near total dependence on imported iron ore, coking coal, and other essential raw materials, which they now receive in bulk cargo carriers as large as 250 thousand DWT. In turn, water transport links the steel plants to world-class shipyards, the latter providing an effective way to turn plates and other steel products into very large ships, high-value-added, manufactured products that are a leading source of export revenue.

Minimills

The Archive’s 51 minimill files contain information on the minimill concept of steel production, its economics in comparison to that of the major mills, technology and plant flows, operating costs, equipment needs and capital costs, DRI-based costs, role in the U.S. steel industry, U.S. plant lists and map, plants in the United Kingdom, financing and financial projections, growth in plant size, feasibility studies, raw-material requirements, original product markets, rod production, role in the flat-rolled steel business, and membership list of the Concrete Reinforcing Steel Institute (CRSI). The files also include documents relating to minimill pioneers Dr. Willy Korf and Nucor’s F. Kenneth Iverson.

Among the Archive’s minimill books and references are the following: Minimills and Integrated Mills: A Comparison of Steelmaking in the United States by Father Hogan; KORF 25 Years: 1955-1980, published by KORF Stahl AG; Economics of the Minimill by Peter Marcus and Karlis Kirsis; and RIVA 1954-1994 by Margherita Balconi. Lists of current and former minimills are contained in a number of references, including the Membership Directory of the Steel Manufacturers Association (SMA), the Directory of the Steel Bar Mills Association (SBMA), and in Metal Bulletin’s Iron and Steel Works of the World.

Analysis: The minimill, a classic example of the way new technology drives competition, emerged in the early 1960’s as a means of exploiting continuous casting, then in the initial stages of its commercial introduction. The first minimills used simple billet-casting machines to link their electric furnaces and flexible rolling mills, which permitted them to enter the steel business on a highly competitive basis for a very limited investment. Their size and approach to production were conducive to simplified corporate and operating structures, much lower overhead costs, and greatly reduced labor inputs relative to their much larger, integrated competitors.

The success of today’s two-million-ton-plus, flat-product minimills makes it easy to forget just how small their early counterparts were and just how little capital they required. In the mid-1960’s, for example, a minimill with 50-60 thousand annual tons of long-product capacity could be built for under $5 million. Just such a plant was built for $4.2 million, land included, by Tennessee Forging Steel Corporation, which in 1966 started up a 60-thousand-ton minimill at Harriman, Tennessee to produce forging-quality billets, rebar, angles, and smooth rounds for sale within a geographic radius of a few hundred miles.

The early success of small minimills in the United States and in Italy, particularly around Brescia, prompted their spread to other parts of Europe, Canada, Japan, the Middle East, Latin America, and Southeast Asia, helping to boost the world’s electric-furnace steel output from 38 million tons in 1960 to 87 million tons in 1970. Then, as continuous-casting technology advanced, so did the role of the minimills. Increasing in number and size, their capability extended to the entire long-products segment, which they came to dominate in most parts of the world.

By 1984, there were 330 minimills worldwide, the top-three minimill countries being Italy with 75, the United States with 50, and Japan with 25. Minimill size, contrary to name and concept, had graduated upward, the capacities of many minimills then exceeding 300 thousand annual tons and directed at producing more diverse and sophisticated products to serve wider geographic markets. As the prospects for added growth in long-product markets began to wane, minimills started to seriously consider the possibility of entering the flat-rolled business.

In 1986, Nucor Corporation was on the verge of installing its first “thin-slab” caster at Crawfordsville , Indiana , having selected new technology developed by Schloemann-Siemag (SMS). Nucor’s breakthrough came with the August 1989 startup of Crawfordville’s new minimill, having an initial capacity to produce 907 thousand annual tons of hot-rolled sheets. Additional minimills in the United States and other countries have since entered the flat-rolled business, and Nucor now operates four thin-slab plants with a combined sheet capacity of about 10 million annual tons, helping to make the company the largest steel producer and scrap recycler in the United States .

Productivity